As Red Sea disruptions intensify, container shipping spot rates are rising on the other side of the globe: for cargo shipped from Asia to the U.S. West Coast.

The Red Sea crisis coincides with drought restrictions in the Panama Canal. Asian cargo bound for East and Gulf Coast ports had previously been switched from Panama to the Suez Canal, and is now being rerouted on even longer voyages around the Cape of Good Hope.

The much shorter route from Asia to the West Coast is looking increasingly attractive.

At 14 knots, a direct voyage from Shanghai to New York via the Cape of Good Hope takes 43 days, according to Sea-Distances.org. A direct voyage from Shanghai to Los Angeles takes only 17 days (plus additional time for cross-country land transport).

The question now is how long Panama and the Red Sea disruptions will persist, giving new strength to Asia-West Coast spot rates.

Annual trans-Pacific contracts generally run from May 1-April 30 and are negotiated in February-April. If trans-Pacific spot rates are supported for months, not weeks, disruptions could push annual contract rates higher.

Asia-West Coast rates up double digits

The Drewry World Container Index (WCI) assessed Shanghai-Los Angeles spot rates at $2,726 per forty-foot equivalent unit for the week ending Thursday, a jump of 30% from the prior weekly reading (Dec. 21, due to the holiday break).

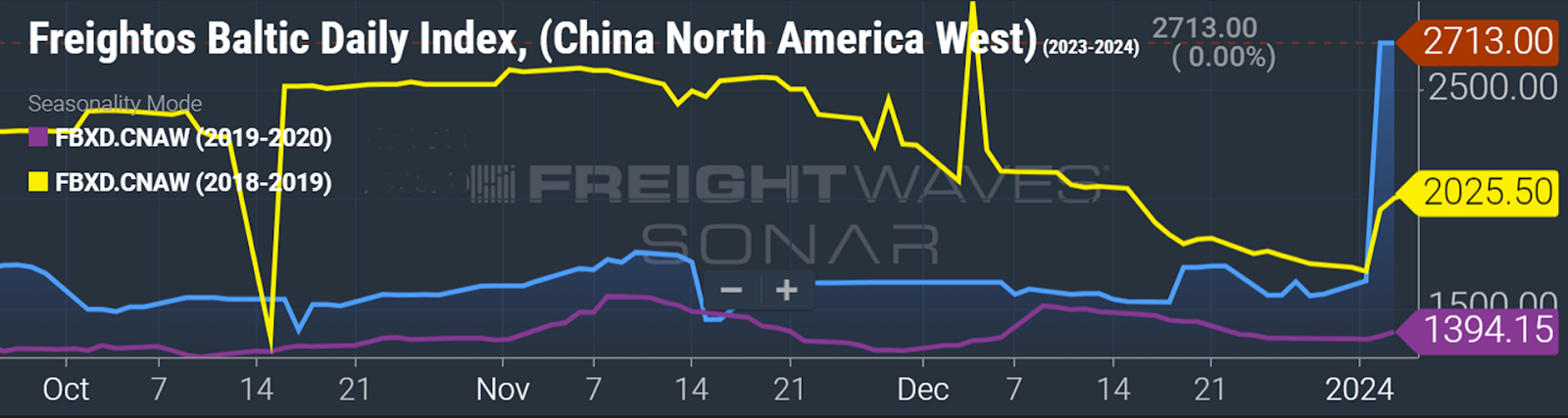

The Freightos Baltic Daily Index (FBX) put China-West Coast rates at $2,713 per FEU on Wednesday. Compared to pre-COVID levels, the current FBX reading is now 34% above rates at this time of year in 2019 and 95% higher than rates in early January 2020.

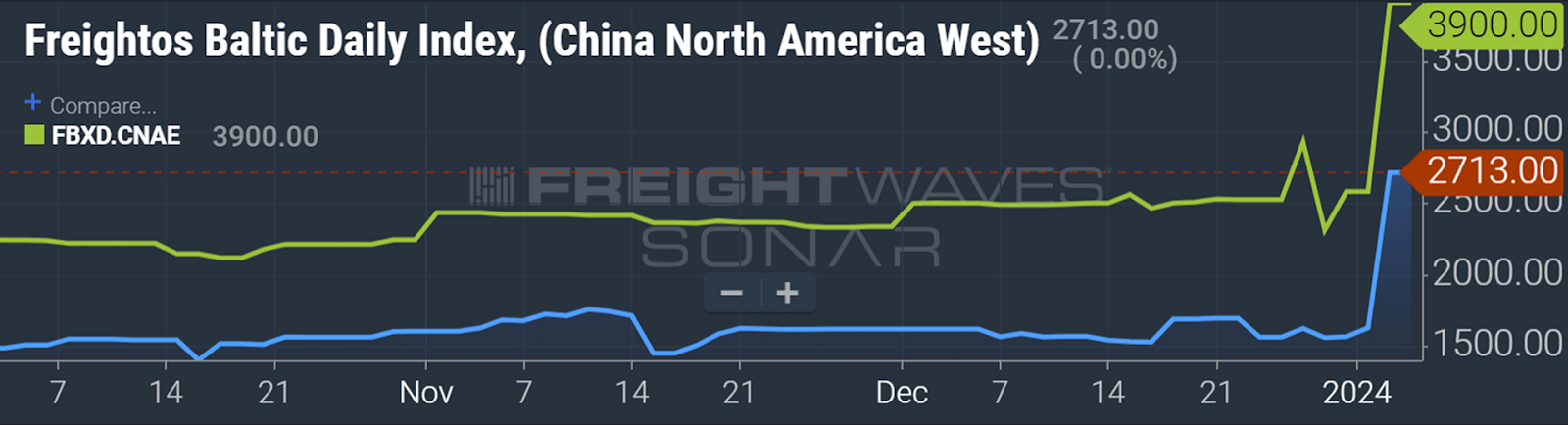

The FBX China-West Coast index surged 73% between Monday and Wednesday. The FBX China-East Coast index — which is directly exposed to Panama and Red Sea issues — was at $3,900 per FEU on Wednesday, up 51% from Monday.

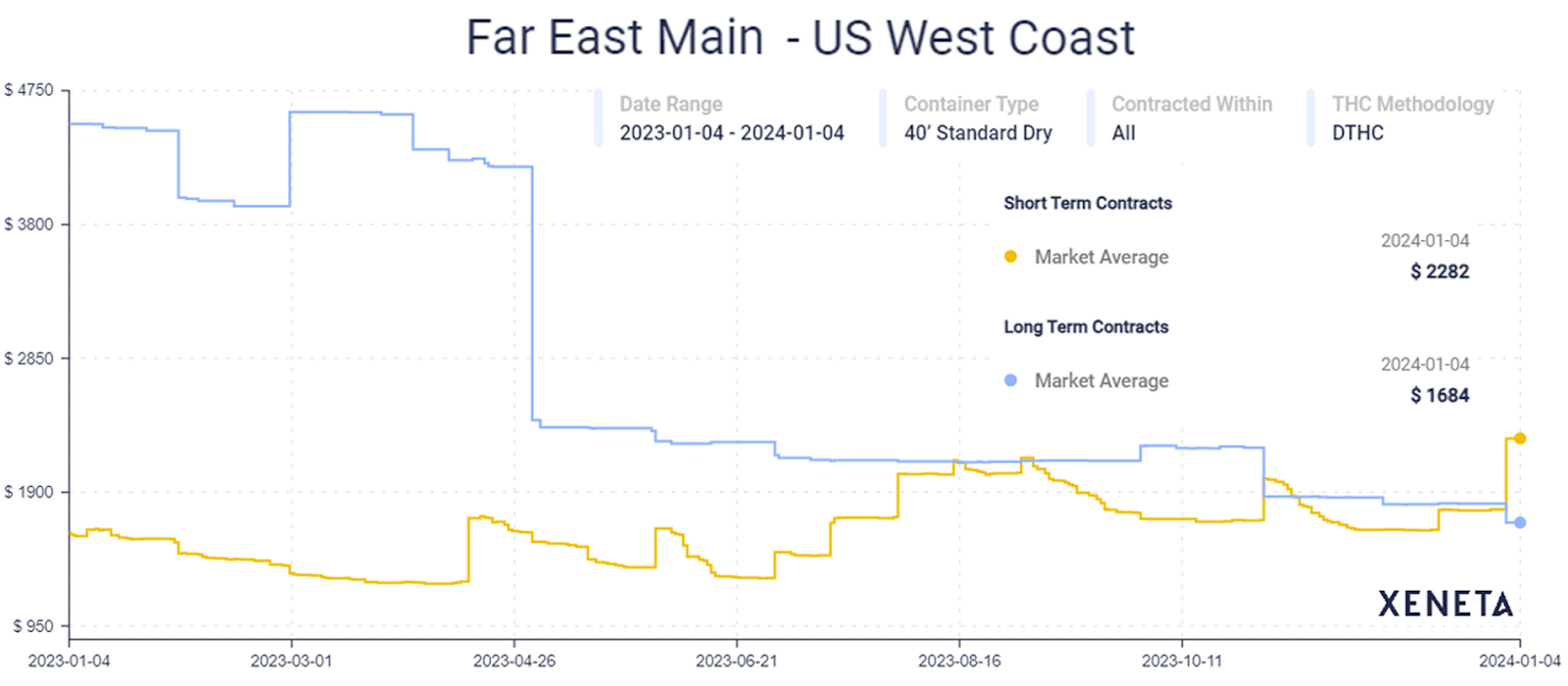

Xeneta tracks both short-term (spot) and long-term (contract) rates. Its data showed average Far East-West Coast spot rates of $2,282 per FEU on Thursday, up 28% from Sunday.

Far East-West Coast contract rates exceeded spot rates for virtually all of 2023, even as annual contract rates reset much lower last spring, according to Xeneta data. However, after the recent spike, average spot rates are now 36% higher than average long-term rates in this lane (for all contracts still in place, including those signed during the last round of annual negotiations).

Will disruptions boost trans-Pacific contract rates?

Whether recent West Coast spot rate gains hang on long enough to boost annual trans-Pacific contract rates that renew in May hinges on the duration of Red Sea and Panama Canal disruptions.

The Red Sea situation is highly uncertain. On Wednesday, a U.S.-led military coalition issued a final warning to the Houthis, implying that ground strikes in Yemen could be imminent. There was yet another security incident on Thursday; a Houthi seaborne drone laden with explosives detonated in the Red Sea.

Meanwhile, Panama Canal restrictions look almost certain to extend through the trans-Pacific contract negotiation period, despite higher-than-expected rainfall in November that prompted a modest increase in transit reservation slots for this month and February.

Panama is currently in the midst of its dry season. The next rainy season begins in May, by which time annual trans-Pacific contracts will have already been signed.

“Come May of 2024, the rainy season will restart and that is the time horizon we have been working for,” said Ricaurte Vásquez Morales, the head of the Panama Canal Authority (ACP), in a presentation in late December.

“Everything we do as far as scheduling, reduction of transits, adjusting advisories and regulations, allocation of slots and everything else we do to manage capacity is geared toward operating the canal throughout the dry season. When the rainfall restarts we will normalize our operations, depending on the actual precipitation we see.”

Deutsche Bank: ‘A short-term phenomenon’

Amit Mehrotra, transport analyst at Deutsche Bank, does not believe the current rate strength is sustainable.

“We believe upward pressure on rates will be a short-term phenomenon based on the overall container freight environment, which remains challenged,” Mehrotra cautioned in a research note on Thursday.

“Based on the latest orderbook and delivery schedule, we expect net fleet growth of 7-8% in 2024 and 5-6% in 2025 [while] ton-mile demand growth is likely to increase by just 3-4% in 2024 and 3-4% in 2025.

“In other words, we don’t believe we are returning to any multi-quarter or multi-year container freight cycle like we saw during the pandemic. While the current situation may be positive for freight rates in the short term, this is happening against a larger backdrop of a weaker container freight market.”

Regarding the Red Sea crisis, Mehrotra said, “Geopolitically, the U.S., Europe, Egypt, China, etc. all have a vested interest in ensuring the free flow of energy commodities and containerized goods through the Suez Canal. Given the number of self-interested parties wanting stability in the region, we think it is only a matter of time [before] some stability is enforced.”